The beverage packaging industry is witnessing a plethora of changes, driven by consumer concern for environmental protection. As awareness about the environment increases, thanks to 24x7 discussions on social media and the internet, consumers are demanding products and services that are in tune with their outlook.

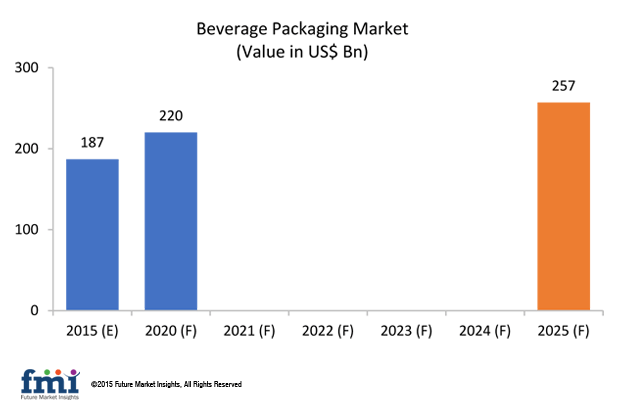

Globally, the valuation of beverage packaging is expected to reach US$ 187 billion by the end of 2015. Owing to strong demand from the beverage industry, which itself is expected to witness stellar growth, the beverage packaging market is expected to reach US$ 220 billion by 2020.

Consumer Experience at the Forefront of Innovation in Beverage Packaging

Consumer experience is a key trend driving the innovation in the beverage packaging sector. The modern-day consumer is not merely content with an impressive design; he desires enhanced functionality, with sustainability being a key focus. Consumer preference for sustainable products can be gauged from Asia Pulp & Paper’s (APP) survey which found that nearly 42% of respondents were willing to pay more for such packaging.

The sustainability trend is expected to become more pronounced in the near future, as discussions on climate control and global warming become more mainstream. More brands will join the organic bandwagon, whereas those who are already doing it are expected to innovate in style and design.

Time constraints are fuelling the demand for drinks that one can have while on the go. Ease of use and convenience have become key focus area for manufacturers. The packaging industry has responded to the demand from city dwellers by offering sturdy, compact, and lightweight packaging.

As more villages transform into suburban areas, and more people move from suburbs to cities, consumption patterns are witnessing a sea-change. In contrast to the “stocking up” trend in villages, people in urban areas prefer to buy smaller packs that serves their “ad-hoc” needs.

Plastic: The Most Preferred Raw Material

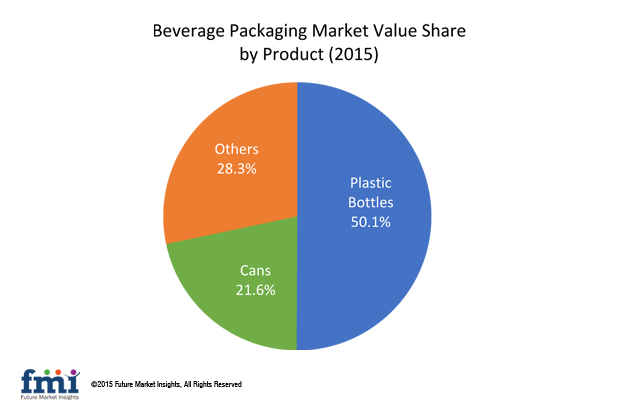

Among the various raw materials used in the manufacture of beverage packaging, plastics are expected to remain the most preferred. Demand for plastics was nearly 31% of all raw materials in 2014. Surging popularity of PET bottles are expected to create sustained demand for plastics in the packaging manufacture industry. Additionally, PET is highly sustainable as it conserves fossil fuel, reduces energy usage and reduces GHG (green house gas) emissions while recycling. Among all the raw materials, only plastics are expected to gain a positive BPS in the next decade.

The key end-products in the beverage packaging market include glass bottles, plastic bottles, cans, liquid cartons, and pouch sachets. Plastic bottles account for nearly half of all the end-products in the beverage packaging market. This growth is attributed to its convenient storage format coupled and wide availability in various shapes and sizes for various applications. Innovation in plastic beverage packaging, such as manufacture of plastic bottles for beer packaging is anticipated to provide growth opportunities for manufacturers.

Among the various types of plastic bottles available in the market, majority are used for packaging CSD/soda. This segment represented nearly 40% market share in the plastic category in 2014. Other key segments include energy drinks and mineral water.

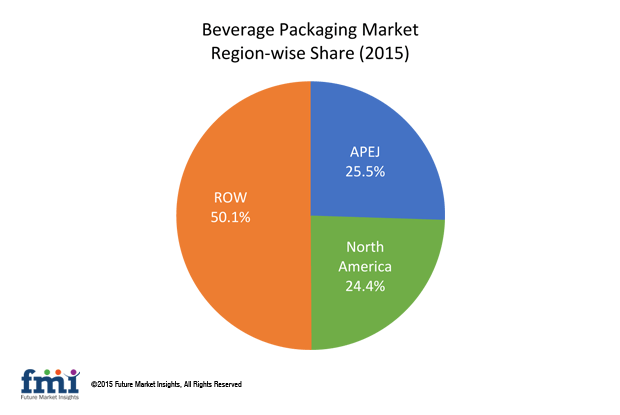

Asia Pacific Excluding Japan (APEJ) Most Lucrative Market

Asia Pacific Excluding Japan (APEJ) is the most lucrative market for beverage packaging, representing nearly one-fourth of the global market in 2014. Demand for beverage packaging in APEJ is expected to be worth US$ 48 billion by the end of 2015. Other key regions for beverage packaging market are North America and Europe.